|

|

|

|

|||||

|

|

|

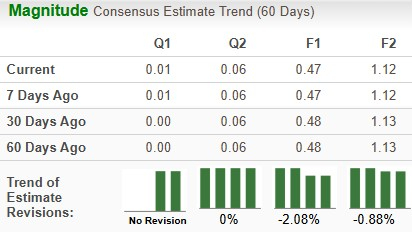

Intel Corporation INTC is scheduled to report its first-quarter 2025 earnings on April 24, after the closing bell. The Zacks Consensus Estimate for sales and earnings is pegged at $12.32 billion and a penny per share, respectively. Over the past 60 days, estimates for INTC have declined to 47 cents per share from 48 cents for 2025 and decreased from earnings of $1.13 per share to $1.12 per share for 2026.

The leading semiconductor manufacturer delivered a four-quarter earnings surprise of negative 366.64%, on average, beating estimates only twice. In the last reported quarter, the company’s earnings surprise was 8.33%.

Our proven model predicts a likely earnings beat for Intel for the first quarter. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is exactly the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Intel currently has an ESP of +400.00% with a Zacks Rank #3. (See the Zacks Earnings Calendar to stay ahead of market-making news.)

You can see the complete list of today’s Zacks #1 Rank stocks here.

During the quarter, Intel announced the launch of a cutting-edge AI solutions suite called Intel AI Edge Systems, Edge AI Suites and Open Edge Platform software. The solutions are designed to simplify the integration of AI at the edge for a wide range of sectors, including manufacturing, retail, media, entertainment and smart cities. The solutions efficiently address industry-specific challenges of enterprises, accelerate the deployment process, and foster innovation in edge AI.

The company introduced Intel Xeon 6 processors with Performance-cores (P-Cores) to cater to the huge demand for high AI workloads across diverse sectors. With industry-leading performance across data center workloads and up to two times higher performance in AI processing, the Xeon 6 family delivers the industry’s best CPU for AI at a lower total cost of ownership. Intel also unveiled Intel Core Ultra processors engineered to redefine mobile computing for a wide range of use cases, such as gaming, content creation, IT applications and various other businesses. This state-of-the-art lineup brings significant advancements in AI capabilities, improved performance and efficiency, setting new standards for AI computing.

Intel also gained two new defense industrial base customers, Trusted Semiconductor Solutions and Reliable MicroSystems, under the U.S Government’s Rapid Assured Microelectronics Prototypes - Commercial initiative. These factors are likely to have a favorable impact on Intel’s upcoming results.

However, in the innovation front, Intel is currently playing a catch-up game with NVIDIA Corporation NVDA, whose H100 and Blackwell graphics processing units are runaway successes. The company is also facing stiff competition from Advanced Micro Devices, Inc. AMD in the commercial PC market.

Despite AI traction, Intel is witnessing declining trends in the Client Computing Group (CCG) owing to inventory adjustments and macroeconomic headwinds. The Zacks Consensus Estimate for revenues from the CCG is pegged at $6.85 billion. Our model projects revenues of $6.89 billion, indicating an 8.5% decline year over year. Intel’s Datacenter and AI Group (DCAI) is plagued by stiff competition. The Zacks Consensus Estimate for revenues from the DCAI is pegged at $2.96 billion. Our model projects revenue of $2.96 billion, indicating a 2.4% decline year over year.

China is the single largest market for Intel. Beijing is accelerating efforts to reduce reliance on Western technology and aiming to phase out foreign chips from key telecom networks by 2027. This shift by the communist nation poses a major challenge for Intel.

Over the past year, Intel has lost 45% against the industry’s growth of 10.3%, lagging its peers like NVIDIA and Advanced Micro Devices.

From a valuation standpoint, Intel appears to be relatively cheaper than the industry and below its mean. Going by the price/sales ratio, the company shares currently trade at 1.51 forward sales, lower than 9.78 for the industry and the stock’s mean of 2.58.

Intel is the only major U.S.-based designer and manufacturer of advanced semiconductor solutions and has been a long-trusted strategic partner of the Department of Defense. Amid growing geopolitical volatility worldwide, the U.S. Government is placing a stronger emphasis on semiconductor self-sufficiency. This presents strong growth potential for Intel. Additionally, the company’s plan to spin off its venture capital business, Intel Capital to focus on core operations and improve liquidity are positive factors.

Intel is steadily diversifying its portfolio with AI at its core to support a vast array of use cases such as IT applications, content creation, and the gaming market. Additionally, Intel Core Ultra processors offer greater scalability, energy efficiency and impressive performance at the edge for autonomous vehicles and industrial IoT applications. Strategic collaboration with major PC makers like Microsoft will likely strengthen its position in the emerging market of AI PCs.

However, Intel is playing a catch-up game with NVIDA and AMD in AI chips and GPU markets. Intensifying competition in the server, storage and networking markets are weighing on margin. Its high reliance on China is exposing it to growing Sino-U.S. trade hostilities, which can significantly impact its financial results. Moreover, its high debt levels may limit sufficient cash flow generation and undermine innovation initiatives.

Intel is undertaking various strategic decisions to gain a firmer footing in the expansive AI sector. It has made significant strides in its cost-cutting plan to rebuild a sustainable growth engine. Efforts to streamline operations, drive efficiency, and the growing clout in AI PC, software, IoT & ADAS domains are positive.

However, with a Zacks Rank #3, Intel appears to be treading in the middle of the road, and new investors could be better off if they trade with caution. Declining earnings estimates, declining share price performance compared to its peers highlights dwindling investors’ confidence.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 3 hours | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 |

Dow Jones Futures: Trump Tariffs Spark Stock Market Sell-Off; Apple, Nvidia, Tesla Are Key Movers

NVDA

Investor's Business Daily

|

| Feb-23 |

Stock Market Today: Dow Sinks As EU Makes Trump Tariff Move; IBM Dives On This AI Threat (Live Coverage)

NVDA

Investor's Business Daily

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite