|

|

|

|

|||||

|

|

|

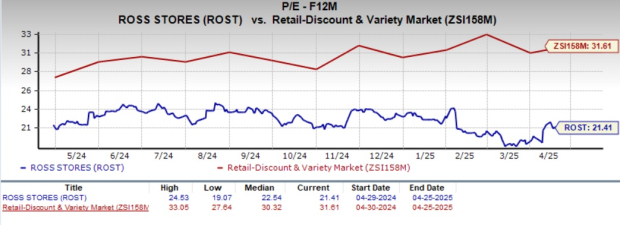

Ross Stores, Inc. ROST is currently trading at a discount relative to its industry peers. The stock trades at a forward 12-month price-to-earnings (P/E) ratio of 21.41X, lower than the industry’s average of 31.61X. Adding to its appeal, ROST holds a Value Score of B, highlighting its strong fundamentals and making it an attractive opportunity for long-term, value-focused investors.

When compared to major discount retailers like Costco Wholesale Corporation COST, Burlington Stores, Inc. BURL and The TJX Companies, Inc. TJX, ROST’s valuation becomes even more compelling. Costco Wholesale, Burlington Stores and TJX Companies are all trading at higher forward P/E ratios of 51.07X, 23.14X and 27.93X, respectively.

Although some investors remain cautious about ROST's short-term potential, its robust fundamentals and recent strong performance point to further upside ahead.

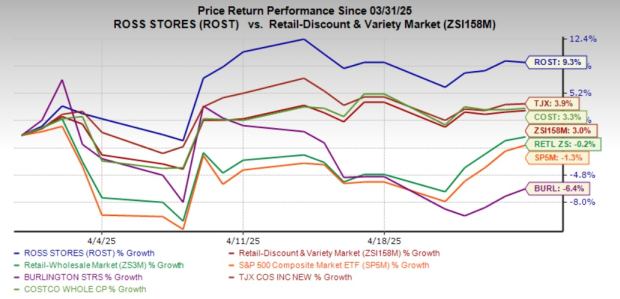

ROST stock has been trending up the charts, recording growth of 9.3% in the past month. This upside outpaces the broader Retail-Wholesale sector’s marginal decline of 0.2% and the Zacks Retail - Discount Stores industry's 3% growth in the same period. Its shares also outperformed the S&P 500 index’s dip of 1.3% in the same timeframe.

Among its discount retail peers, Ross Stores' stock performance stands out. Over the past month, shares of The TJX Companies and Costco Wholesale gained 3.9% and 3.3%, respectively, while Burlington Stores lost 6.4%.

Ross Stores continues to benefit from strong customer response to its merchandise across both banners, driving a 3% improvement in comparable store sales (comps) in fourth-quarter fiscal 2024. This growth was primarily fueled by increased customer traffic and larger basket sizes, reflecting a rise in the number of shoppers and the volume of purchases per visit. Consequently, sales grew 3% year over year in the fiscal fourth quarter.

The company’s proven business model emphasizes competitive bargains, making its stores appealing destinations across various economic conditions. Additionally, its off-price model delivers a strong value proposition and leverages micro-merchandising to optimize product allocation and improve margins.

This strategy ensures that ROST delivers in-demand products while maintaining cost efficiency, which resonates well with budget-conscious shoppers. The continued focus on offering designer and branded goods at discounted prices has helped Ross Stores maintain its competitive edge amid massive economic pressure.

Ross Stores has been consistent with the execution of its store expansion plans over the years. The company’s store expansion efforts are focused on continually increasing penetration in the existing and new markets. It intends to add 19 stores, consisting of 16 Ross and three dd's DISCOUNTS, in the first quarter of fiscal 2025. For fiscal 2025, management expects to open roughly 90 locations, comprised of about 80 Ross and 10 DDs. Such openings do not reflect plans to close or relocate about 10 to 15 older stores.

Reflecting positive sentiment around ROST stock, the Zacks Consensus Estimate for earnings per share for fiscal 2025 and 2026 has risen 1.4% and 7.8%, respectively. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

Despite its strengths, following a strong holiday season, sales trends softened in late January and February due to macroeconomic volatility, rising inflation and geopolitical uncertainty, which weighed on consumer confidence and discretionary spending. Additionally, unseasonable weather impacted store traffic.

Given these external pressures, Ross Stores has adopted a cautious outlook for fiscal 2025. For the fiscal first quarter, management expects comparable store sales between a 3% decline and flat, compared with 3% growth in the prior-year quarter. Total sales are projected to be down 1% to up 3% year over year, with operating margin forecasted between 11.4% and 12.1% (down from 12.2% a year ago). Merchandise margin is expected to decline slightly.

For the fiscal first quarter, Ross Stores anticipates comps between a 1% decline and a 2% increase. Excluding a one-time gain, the operating margin forecast reflects sales deleverage, increased distribution costs and lower incentive compensation expenses.

Investors should consider Ross Stores stock for its strategic focus on value-oriented off-price retailing, delivering branded and designer goods at discounted prices. This approach has helped ROST maintain a competitive advantage and align with its long-term growth goals.

However, management acknowledges the pressure facing its core customer base, primarily low-to-moderate-income shoppers, who are grappling with persistently high costs for essentials. This economic strain could restrict discretionary spending in the near term, affecting sales growth. Currently, the stock has a Zacks Rank #3 (Hold), reflecting a balanced outlook for its future performance.You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite