|

|

|

|

|||||

|

|

|

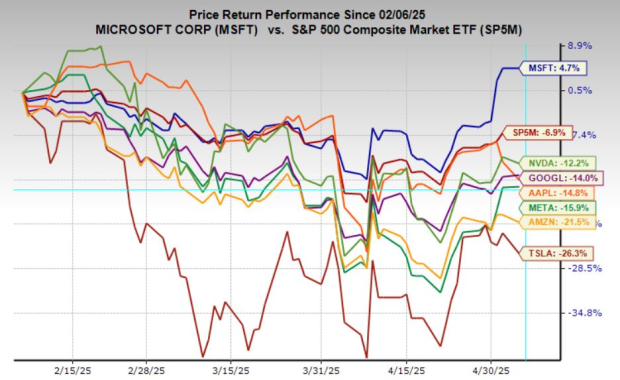

Over the past two weeks, most of the Magnificent 7 have reported earnings, and the results were broadly positive, reinforcing the strength and scale of these market leaders. Last week brought reports from Amazon (AMZN), Apple (AAPL), Meta Platforms (META), and Microsoft (MSFT), while the prior week featured Alphabet (GOOGL) and Tesla (TSLA).

Among them, one company quietly stood above the rest: Microsoft.

Microsoft’s earnings results aren’t the only thing prompting me to highlight the stock either—MSFT also boasts the highest Zacks Rank of the Mag 7 group, with a Zacks Rank #2 (Buy) and has been the best performing stock over the last one month, three months and year-to-date of the group.

Microsoft’s cloud business was the clear standout this quarter. Azure revenue grew 33% year-over-year, which was the fastest among the three major cloud providers, with AI services alone contributing 12 percentage points to that growth. The broader Intelligent Cloud segment reported $26.8 billion in revenue, up 21% from the prior year, with operating income reaching $11.1 billion.

By comparison, Amazon Web Services (AWS) posted revenue of $29.3 billion, maintaining its lead in scale but growing just 17%, it marked the slowest pace of growth in five quarters. While AWS remains highly profitable, with a record 39.5% operating margin, the slowdown raises questions about whether it's ceding growth momentum to competitors.

Google Cloud also delivered strong results, with revenue up 28% year-over-year to $12.3 billion. Operating income came in at $2.2 billion, a significant improvement from $900 million a year ago, showing continued progress toward profitability.

Taken together, these results highlight Microsoft’s continued leadership in enterprise cloud and its growing advantage in AI infrastructure — both key drivers of long-term value. Azure’s faster growth rate not only reinforces Microsoft’s competitive edge, but also reflects its broader strategic positioning in what remains one of the most critical areas of tech spending.

As US–China trade tensions rise, tariff exposure has become a key risk factor for large-cap tech investors. Among the Magnificent 7, Microsoft is uniquely positioned, not only due to its strong fundamentals, but also because of its relatively low exposure to China and tariff-related disruptions.

Apple stands out as one of the most vulnerable. The company’s reliance on Chinese manufacturing for iPhones, iPads, and other hardware makes it especially sensitive to rising import costs and potential supply chain snarls. A significant portion of Apple’s revenue also comes from Chinese consumers—a market that could easily be affected by retaliatory measures.

Amazon faces its own set of challenges. While its core North American business remains robust, the company’s global retail supply chain depends heavily on low-cost manufacturing hubs in China. Tariffs on goods shipped to the US from China could squeeze margins or complicate logistics for its sellers.

Meta Platforms is less directly exposed to supply chains but faces its own geopolitical and macro risks. The company has long been restricted in China, but it still relies on global ad spending from brands with supply chains and customer bases in the region. In a deteriorating US–China trade environment, global advertising spend could weaken, affecting Meta’s growth.

Microsoft, by contrast, benefits from a business model centered around software, cloud infrastructure, and enterprise services, which are less vulnerable to tariffs or localized trade friction. Its supply chain exposure to China is limited, and its revenue is globally diversified, with much of its growth coming from the US, Europe, and emerging AI-driven demand.

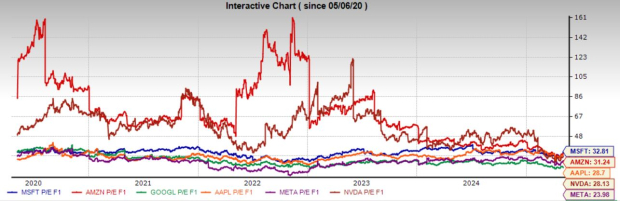

Microsoft currently holds the highest earnings multiple among the Magnificent 7, but that premium may be well-earned. While MSFT trades above its peers, it remains in line with its five-year median earnings multiple and so do Apple and Meta, which suggests that valuations are fair from a historical perspective.

The rest of the group is trading well below their five-year averages, a welcome development for valuation-conscious investors after the sharp run-ups in recent years. Importantly, these valuations come alongside healthy earnings growth forecasts, which range from 12.8% annually for Apple to as high as 24.7% for Nvidia. Microsoft is expected to grow its earnings 14.6% annually over the next three to five years.

With Microsoft’s strong competitive positioning, durable growth, and relatively low macro risk, its premium multiple appears justified, however, most of the Magnificent 7 stocks appear attractively valued.

Microsoft continues to stand out as a well-rounded member of the Magnificent 7—delivering top-tier cloud growth, strong earnings momentum, and relatively low exposure to macro and geopolitical risks. Its premium valuation appears justified given its leadership in AI and enterprise business, and its stock performance reflects growing investor confidence.

While many of its peers also look attractively valued after recent pullbacks, Microsoft remains a compelling core holding for long-term investors seeking stability, growth, and resilience in an uncertain market.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 17 min | |

| 52 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours |

Mark Zuckerberg Grilled on Usage Goals and Underage Users at California Trial

META

The Wall Street Journal

|

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite