|

|

|

|

|||||

|

|

|

Chevron Corporation CVX released its first-quarter 2025 earnings last Friday, posting results that beat on the bottom line but missed on the top. Adjusted earnings came in at $2.18 per share, slightly above expectations but down 26% from a year ago. Revenues fell 2.3% year over year to $47.6 billion, missing estimates as well. These results were met with a muted reaction, as investors continue to weigh the mixed signals from the oil supermajor’s earnings report, valuation and broader macro environment. (Find the latest earnings estimates and surprises on Zacks Earnings Calendar.)

Currently trading just above $135 — dangerously close to its 52-week low of $132.04 — Chevron’s stock has struggled. Over the past three years, shares are down around 15%, sharply underperforming rival ExxonMobil XOM, which has gained 24% in the same period. This stark divergence has left investors questioning Chevron’s positioning, especially given the ongoing pressures in the energy market, geopolitical uncertainties and a looming arbitration case over its proposed acquisition of Hess Corporation HES.

Let’s take a closer look at the broader landscape.

While Chevron delivered a solid earnings beat, the quality of that beat is up for debate. The strength came largely from higher-than-expected U.S. natural gas production, while oil realizations and margins in the refining segment disappointed. Upstream earnings fell 28.3% year over year, primarily due to weaker oil prices and flat production levels. In the downstream segment, profits slumped nearly 60% due to lower margins. Free cash flow was $1.3 billion, significantly below the prior-year levels, although the company still managed to return $6.9 billion to its shareholders through dividends and buybacks.

Chevron has also trimmed its second-quarter buyback target to $2.5-$3 billion, down from $3.9 billion in Q1, a move that reflects the shaky macro landscape and Brent crude’s slide toward $60. The lower buyback pace raises questions about the sustainability of Chevron’s capital return strategy if commodity prices stay subdued.

One reason investors are still paying attention to Chevron is its high-quality asset base. The company continues to benefit from strong operational performance in the Permian Basin, where around 80% of its acreage carries low or no royalty obligations. This improves long-term returns and supports production efficiency. The Tengiz field in Kazakhstan and new deepwater projects like Ballymore in the Gulf of America further strengthen its production profile.

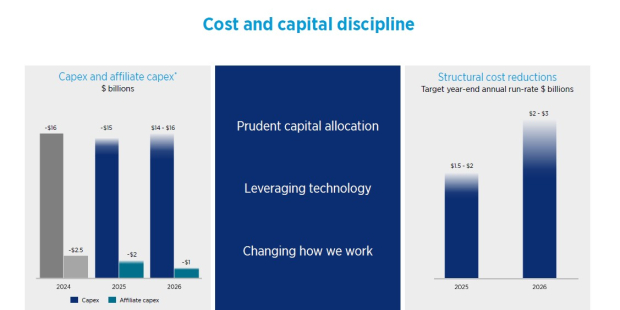

On the cost side, Chevron’s capital discipline is commendable. The company has kept capex tight, spending just $3.9 billion in Q1 while progressing on major projects. It’s also pursuing a $2–$3 billion cost reduction initiative through 2026. With a debt-to-capital ratio of around 16.6, Chevron’s balance sheet remains one of the healthiest among global oil majors.

Notably, Chevron is still guiding for $10-$20 billion in annual share buybacks, though execution will depend heavily on commodity prices. The company also offers a solid dividend yield of 5%, with 38 consecutive years of dividend growth—a reassuring point for income-focused investors.

One major overhang on the stock is the pending $53 billion acquisition of Hess. The prize is Hess’s 30% stake in the Stabroek block offshore Guyana, a prolific oil discovery operated by ExxonMobil. However, ExxonMobil and its partner CNOOC have taken Chevron to arbitration, claiming a right of first refusal. The outcome of the arbitration, with hearings set for late May, could determine whether Chevron’s biggest growth catalyst materializes or not.

If the deal fails, Chevron will miss out on a major addition to its reserves and production. But management maintains that even without Hess, it has the project pipeline and financial strength to deliver growth. Still, the uncertainty adds headline risk that investors must monitor closely.

The backdrop isn’t particularly supportive for Chevron either. Falling oil prices—due to global trade tensions, potential demand weakness, and OPEC+ developments—have put pressure on upstream earnings. Over the past week, the Zacks Consensus Estimates for Chevron’s 2025 and 2026 earnings have both moved downward, signaling waning confidence in the near-term outlook.

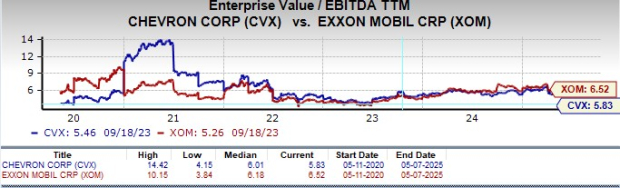

However, valuation does offer some cushion. Chevron trades at an EV/EBITDA multiple of 5.83, which is appealing relative to ExxonMobil and below its five-year historical average. The company also holds a Zacks Value Score of B, suggesting that long-term investors looking for a well-managed energy play may still find value here.

Chevron’s Q1 performance reflects both its strengths and its current challenges. It continues to execute well on cost control and operational efficiency while maintaining a shareholder-friendly capital return program. At the same time, macro headwinds, declining oil prices, the Hess arbitration uncertainty, and slowing buybacks cloud the near-term outlook.

Given the company’s strong balance sheet, disciplined capital management, and fair valuation, but also its muted growth prospects and legal overhang, CVX stock appears appropriately priced for now. Investors might consider holding existing positions while waiting for greater clarity on oil prices, the Hess deal outcome, and future earnings trends. For these reasons, Chevron stock is currently a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 8 hours | |

| 12 hours | |

| Feb-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite