|

|

|

|

|||||

|

|

|

Ford F and Toyota TM are two well-recognized names in the global auto industry and fierce rivals in the U.S. market. Toyota, the Japanese heavyweight, currently holds the No. 2 spot in the U.S. market, selling 2.33 million vehicles last year. That’s a 3.7% increase from 2023. Not far behind is Ford, the homegrown challenger, with 2.07 million vehicles sold, up 4.2% year over year.

But the gap widens on a global scale. Toyota’s massive reach helped it move 10.8 million vehicles worldwide in 2024, while Ford sold just 4.5 million. That difference is visible in their market caps too — Toyota is valued at around $250 billion, compared to Ford’s $40 billion.

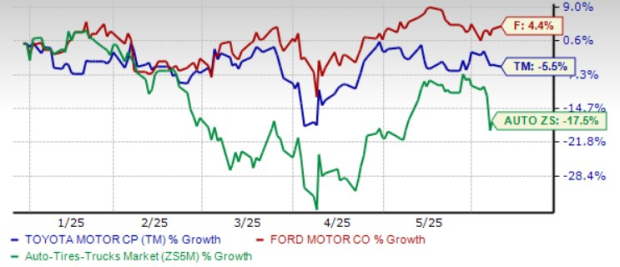

Year to date, shares of Toyota have declined 5.5%, while Ford has grown 4.4%. Nonetheless, both have outperformed the auto sector over the same timeframe.

So, which stock is the better pick right now? Let’s dig into the fundamentals, growth drivers, and potential risks to see which automaker deserves a spot in your portfolio.

Ford remains a key player in the U.S. auto market, with a lineup that continues to resonate with American buyers. The F-Series trucks continue to be a best-seller, and models like the Maverick pickup, Escape, Explorer, Expedition, and Edge keep Ford well-positioned in the SUV and crossover space.

The company’s hybrid strategy is paying off. As full EV adoption slows, hybrids are gaining traction. Ford’s growing hybrid sales give it a nice middle ground—appealing to buyers who want better fuel efficiency without fully committing to electric.

Financially, Ford is in a relatively strong position. The company exited the first quarter of 2025 with $27 billion in cash and $45 billion in liquidity. This provides room to invest in its Ford+ priorities, including digital innovation and electrification. Another appealing factor for Ford’s investors is its dividend, which currently yields roughly 6%, much higher than the S&P 500 average. The company also aims to return 40–50% of free cash flow to shareholders, signaling a continued focus on income investors.

Ford Motor Company dividend-yield-ttm | Ford Motor Company Quote

A major growth engine for Ford is its Ford Pro business, which is focused on commercial customers. With strong demand, a successful Super Duty launch and growing interest in its software and service offerings, Ford Pro could become a real earnings driver. Ford’s push into tech and fleet solutions is showing promise.

That said, Ford faces real challenges. Its traditional gas-powered vehicle unit, Ford Blue, is under pressure. Sales are expected to fall, and foreign exchange issues could further dent profits. Meanwhile, its EV division, Model e, is bleeding money. Losses reached over $5 billion in 2024 and may continue to rise as competition intensifies.

Policy risk is another key concern. U.S. President Trump’s tariffs may cost Ford up to $2.5 billion. While Ford aims to offset $1 billion of this through strategic actions, the remaining $1.5 billion, expected to hit in 2025, remains a major concern. Supply chain disruptions or retaliatory tariffs could further impact operations and demand. These uncertainties, combined with the internal pressure, continue to cloud the near-term picture for the company.

The Zacks Consensus Estimate for Ford’s 2025 sales and EPS implies a year-over-year decline of 7% and 40%, respectively.

Toyota continues to prove why it's often viewed as one of the most dependable names in the global auto industry. The company beat earnings expectations in its last reported quarter and is guiding for growth in both revenues and vehicle volumes for fiscal 2026, which ends March 31, 2026. Despite its strong top-line outlook, Toyota is bracing for some near-term pressure on its profits.

The automaker expects operating income to decline 21% this fiscal year. Several factors are behind this outlook—rising material costs, currency headwinds from a stronger yen and the potential impact of Trump-era tariffs. These tariffs could drive vehicle prices higher, which may cool demand in important markets like the United States.

Still, Toyota is projecting a rise in vehicle sales. It expects to sell 9.8 million vehicles in fiscal 2026, up from 9.36 million sold in fiscal 2025. Including Lexus, total sales could reach 10.4 million units. Electrified vehicles remain a big growth area. Toyota expects to sell 5.18 million hybrids and plug-in hybrids this year, an increase from 4.75 million in fiscal 2025. This strength is helping to support a modest bump in forecasted revenues to ¥48.5 trillion.

Toyota’s hybrid-first approach continues to gain traction. A clear example is RAV4 — America’s top-selling SUV — which will be sold only as a hybrid or plug-in hybrid starting in 2026. While rivals rush to go all-in on battery electrics, Toyota is sticking to a more gradual and cost-effective path. It’s also exploring alternative solutions like hydrogen, with a focus on commercial vehicles and building out infrastructure to lower costs over time.

For shareholders, the company has remained consistent. Toyota raised its annual dividend to 90 yen per share in fiscal 2025 and plans to increase it further to 95 yen in fiscal 2026. Between its cautious electrification strategy and steady capital returns, Toyota continues to navigate a changing auto industry with discipline, even as headwinds build.

The Zacks Consensus Estimate for Toyota’s fiscal 2026 sales indicates 8% growth year over year, while earnings are expected to decline 21%.

In a capital-heavy industry like autos, evaluating how efficiently a company puts its money to work is key. On that front, Toyota holds an edge.

Toyota’s return on invested capital stands at 4.8%, well above Ford’s 1.77%. While neither figure is particularly strong in absolute terms, the gap suggests that Toyota is more effective at generating profit from its capital base.

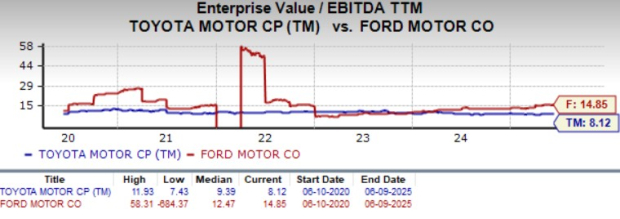

On a valuation basis, Toyota trades at a more attractive EV/EBITDA multiple than Ford. This suggests that, relative to its earnings before interest, taxes, depreciation, and amortization, Toyota’s stock is priced more reasonably.

Ford and Toyota are both navigating an evolving auto landscape shaped by electrification, policy risks and shifting consumer demand. Ford has strong brand recognition in the United States, a high dividend yield, and potential upside in its Ford Pro division. However, persistent EV losses, tariff overhang and weaker capital efficiency cloud the near-term outlook.

Toyota, meanwhile, faces its own headwinds—currency and margin pressures. But its global scale, resilient hybrid sales, and cautious approach to electrification offer a more stable path forward. The company is growing volumes without getting weighed down by the high costs of going all-in on EVs.

Add in Toyota’s stronger return on invested capital and more attractive valuation, and the case becomes clearer. While both stocks have a Zacks Rank #3 (Hold) for now, but if forced to pick today, Toyota’s stronger capital discipline and strategic positioning give it a slight edge.

You can see the complete list of today’s Zacks Rank #1 (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| 8 hours | |

| 10 hours | |

| 11 hours | |

| 16 hours | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-14 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite