|

|

|

|

|||||

|

|

|

American Express Company AXP is gaining attention as its earnings estimates for 2025 have moved higher over the past week. The company delivered strong first-quarter 2025 earnings, driven by growing Card Member spending and a premium customer base. Rising revolving loan balances and continued robust card fee growth aided its performance. The results were partially offset by escalating customer engagement and operating costs.

Wall Street analysts are turning bullish on the stock, as evident from the earnings estimates’ northward revision. Over the past seven days, the Zacks Consensus Estimate for 2025 earnings has increased 1 cent.

The Zacks Consensus Estimate for AmEx’s 2025 and 2026 earnings indicates 13.9% year-over-year growth each. Similarly, the consensus mark for 2025 and 2026 revenues is pegged at $71.3 billion and $77 billion, respectively, indicating 8.1% and 8% year-over-year growth.

It beat earnings estimates in each of the past four quarters, with the average surprise being 5.2%.

American Express Company price-eps-surprise | American Express Company Quote

Analysts anticipate that American Express will soon announce a significant increase in the annual fee for its Platinum card, following rival JPMorgan Chase & Co.’s JPM decision to raise the fee on its Sapphire Reserve card by 45% to $795, a record hike among major U.S. credit cards. AmEx is expected to unveil its largest-ever card revamp this fall, marking a substantial investment in its premium offering.

Warren Buffett frequently cites AmEx as a prime example of a durable business with a strong competitive moat. Unlike Visa Inc. V and Mastercard Incorporated MA, which operate solely as payment networks, AmEx also functions as a bank, allowing it to generate revenue from both transaction fees and interest on card balances. This integrated model provides a more diversified income stream and enhances its resilience to economic uncertainty.

The company is also making notable inroads with younger consumers. Gen X, millennials, and Gen Z now represent a significant share of AmEx's customer base, spending at higher levels than baby boomers and driving long-term growth prospects.

Financially, AmEx remains on solid footing. As of the first quarter of 2025, it held $52.5 billion in cash and equivalents against just $1.6 billion in short-term debt. The company returned $7.9 billion to shareholders in 2024 through dividends and buybacks and maintained that momentum in early 2025 with $1.3 billion returned in the first quarter. Additionally, it boosted its quarterly dividend by 17% in March 2025 to 82 cents per share.

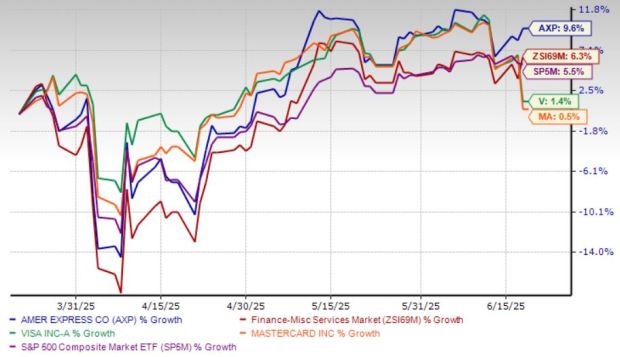

AmEx stock has gained 9.6% over the past three months, underperforming the industry’s 6.3% decline. Peers like Visaand Mastercardalso witnessed growth, but to a lesser extent. Meanwhile, the S&P 500 has gained 5.5% in the same period.

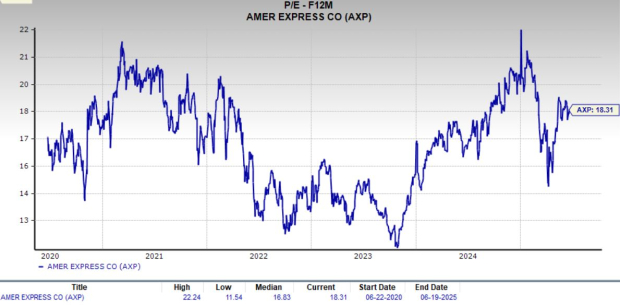

AXP is currently trading at a premium based on its historical valuation. Its forward P/E ratio stands at 18.31X, above its five-year median of 16.83X, indicating a higher-than-usual market confidence in its growth prospects. However, when compared to peers such as Visa and Mastercard, which trade at forward P/E multiples of 27.53X and 31.27X, respectively, AXP appears relatively attractive.

American Express continues to grapple with rising expenses, which could weigh on profit growth. Total costs have climbed steadily in recent years, up 22% in 2021, 24% in 2022, 10% in 2023 and 6% in 2024. The trend persisted into the first quarter of 2025, with expenses rising 10% year over year to $12.5 billion. A large portion of these costs stems from customer engagement and marketing efforts, which are expected to remain elevated, putting pressure on margins.

Reward expenses and cardmember services remain key cost drivers, comprising nearly 45% of total expenses in 2024. These categories are set to rise further as consumer spending grows. Membership Rewards and cashback payouts have increased in line with higher billed business, while surging travel-related expenditure has also contributed to the jump in rewards expenses.

American Express remains fundamentally strong, backed by a premium customer base, diversified revenue streams and a solid balance sheet. Its ability to capture younger demographics and the planned Platinum card revamp offer long-term growth potential. However, rising expenses, especially in rewards and customer engagement, pose margin risks, while the stock’s premium valuation versus its historical average tempers near-term upside potential.

Although analyst sentiment has improved slightly, with upward estimate revisions for 2025, these positive factors appear largely priced in. Given this balanced risk-reward profile, a Zacks Rank #3 (Hold) seems appropriate, suggesting investors wait for a more attractive entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-04 | |

| Apr-04 | |

| Apr-04 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 |

Interview: Boku CEO Stuart Neal on why the UK needs a Mastercard, Visa rival

V MA

Retail Banker International

|

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite