|

|

|

|

|||||

|

|

|

Fortinet FTNT is strengthening its enterprise cybersecurity position through a unified Secure Access Service Edge (SASE) strategy that combines next-generation firewall, SD-WAN, secure web gateway and Data Loss Prevention (DLP) into a single OS, FortiOS. This helps organizations streamline security while cutting complexity and costs. Fortinet also offers sovereign SASE solutions for regulated sectors.

According to Fortinet, the typical SASE journey starts with FortiGate firewalls, then expands to SD-WAN and FortiSASE. By the first quarter of 2025, 73% of large enterprises had adopted Fortinet’s SD-WAN, while FortiSASE penetration rose to 11%, up nearly 10 points sequentially.

In the first quarter, unified SASE billings grew 18% year over year, representing 25% of total billings. Fortinet cited strong momentum across industries, with several major wins displacing incumbent SASE vendors due to better performance, integration and cost efficiency.

Yet, investors should take a closer look at what is working in Fortinet’s favor and what is holding it back, explaining why FTNT stock is a hold for now. Let’s delve deeper into the company’s fundamentals.

Fortinet is strengthening its unified SASE architecture with cloud-native solutions to secure hybrid and multi-cloud environments. Updates to FortiCNAPP and the launch of services like FortiAppSec Cloud, FortiMail Workspace Security, FortiNDR Cloud, FortiSIEM and Incident Response on AWS Marketplace support its cloud-first strategy.

Enhancements to FortiMail and FortiDLP expand protection to browsers and collaboration apps, which are key parts of the Secure Web Gateway and DLP in SASE. These AI-driven, fabric-integrated upgrades will help drive FTNT’s revenues in the near term.

The cybersecurity market is extremely competitive and characterized by rapid technological change. Among others, Fortinet’s competitors include Palo Alto Networks PANW, Zscaler ZS and CrowdStrike CRWD.

Palo Alto Networks has driven growth through strategic partnerships, including an expanded alliance with VMware and collaborations with Aruba Networks and others under its NextWave program. Zscaler has grown via acquisitions like Airgap Networks and Avalor, strengthening its Zero Trust and threat prediction tools. CrowdStrike continues to expand its Falcon platform, now with 29 modules, including Falcon Data Protection and AI-powered XDR features.

These aggressive moves by key rivals highlight the intense competition Fortinet faces in maintaining its market share and growth momentum.

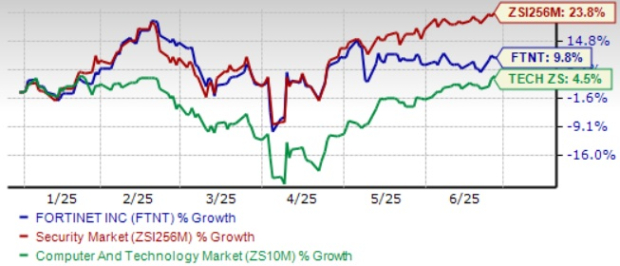

Fortinet shares have gained 9.8% in the year-to-date (YTD) period, underperforming the Zacks Security industry’s growth of 23.8%, but outperforming the Zacks Computer and Technology sector’s return of 4.5%.

Fortinet’s underperformance compared with the industry is driven by rising competitive pressure in the fast-growing cybersecurity space. While progress in AI and SASE offers support, customer hesitancy and macro uncertainties have weighed on investor sentiment.

Shares of Palo Alto Networks, Zscaler and CrowdStrike have returned 12.4%, 73.1% and 44%, respectively, YTD.

Fortinet’s valuation may be a concern for some investors. The stock is trading at a significant premium compared to the broader Zacks Security industry. As of the latest data, FTNT’s Price/Book ratio hovers around 40.40, well above the industry’s 24.95. The Value Score of F further reinforces a stretched valuation for Fortinet at this moment.

Fortinet expects revenues for the second quarter of 2025 in the range of $1.59 billion to $1.65 billion, which suggests growth of 13% at the midpoint. It anticipates non-GAAP earnings per share in the band of 58-60 cents.

Fortinet maintained a cautious outlook for the second quarter, citing macroeconomic and geopolitical uncertainties. While close rates and sales trends remained solid, sales teams were hesitant to raise expectations. The company also noted customer hesitancy in finalizing purchases, prompting a prudent approach to guidance despite steady demand.

The Zacks Consensus Estimate for second-quarter 2025 revenues is pegged at $1.62 billion, suggesting 12.94% year-over-year growth.

The consensus mark for second-quarter 2025 earnings is pegged at 59 cents per share, which has remained steady over the past 30 days, indicating 3.51% year-over-year growth.

Fortinet’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 23.83%.

Fortinet, Inc. price-consensus-chart | Fortinet, Inc. Quote

Fortinet’s strong SASE growth, new cloud-based offerings and expanding customer base show that the company is moving in the right direction. However, tough competition, premium valuation and cautious guidance suggest that the stock may not see major gains in the near term.

While its long-term prospects remain solid, the stock has underperformed compared to the industry and faces clear headwinds due to macroeconomic and geopolitical uncertainties. For now, it makes sense for investors to hold their position and wait for clearer signals before considering fresh entry.

Fortinet currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 6 hours | |

| 7 hours | |

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite