|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Showing signs of a comeback, Intel INTC stock has started to rebound and is up +15% in 2025, with the chip giant’s much-anticipated Q2 results approaching after-market hours on Thursday, July 24.

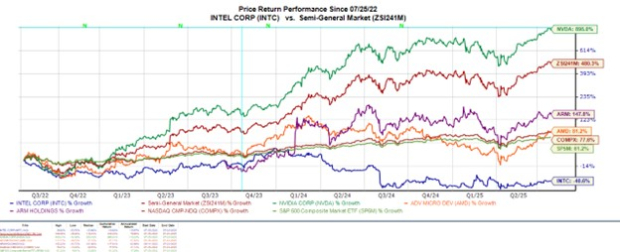

In regard to the anticipation, Intel is still one of the world's largest semiconductor companies but has infamously lost market share to Nvidia NVDA, AMD AMD, and Arm Holdings ARM.

This makes it a very worthy topic of whether it’s time to buy, hold, or sell Intel stock, which is still down 40% over the last three years to vastly trail the broader indexes and its aforementioned competitors.

Although Intel hasn’t given its turnaround strategy a flashy name, optimism has swooned after the company appointed Lip-Bu Tan as its new CEO in March. As a seasoned semiconductor executive who previously served as CEO of Cadence Design Systems CDNS, Tan has simply called Intel’s reemergence plan a “bold turnaround strategy.”

Getting “back to the basics”, Tan’s emphasis has been on refocusing Intel on engineering excellence, streamlining management to place a priority on an engineering-first culture.

Foundry Restructuring: Intel has separated its foundry business into a separate subsidiary called Intel Foundry Services (IFS) to better compete with Taiwan Semiconductor TSM while focusing on its core business as a supplier of microprocessors and chipsets.

Talent Overhaul: The company has hired top engineers from Apple AAPL and Alphabet GOOGL while trimming factory workforce to boost innovation.

Aggressive AI pricing: Intel’s Gaudi 3 AI accelerator is priced significantly lower than Nvidia’s comparable offerings, aiming to disrupt the AI hardware market.

Although Intel has regained some ground in the PC chip market, Q2 sales are thought to have dipped 7% to $11.87 billion compared to $12.83 billion a year ago. On the bottom line, Q2 earnings are expected at $0.01 a share from EPS of $0.02 in the prior year quarter.

Optimistically, Intel’s annual earnings are projected to climb swing to $0.27 per share in fiscal 2025 versus an adjusted loss of -$0.13 a share last year. However, it's noteworthy that FY25 EPS estimates have noticeably declined from projections of $0.50 a share 90 days ago and are slightly down in the last week.

Similarly, Intel’s EPS is forecasted to sharply rebound to $0.70 in FY26, but estimates have also trended lower in the last seven days and have now dropped 37% over the last three months from projections of $1.12 per share.

Unfortunately, despite Intel’s somewhat promising turnaround strategy, the trend of declining earnings estimate revisions does suggest it may be time to fade this year's rally. Correlating with such, Intel stock currently lands a Zacks Rank #4 (Sell), and the chip giant’s Q2 report will be critical to reconfirming what is hopefully a return to prominence at some point.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 26 min | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours |

How Will Dow Jones Futures Open After Trump Hikes Global Tariff To 15%?

AMD GOOGL TSM NVDA

Investor's Business Daily

|

| 5 hours | |

| 6 hours | |

| 7 hours | |

| 9 hours | |

| 9 hours | |

| 9 hours | |

| 9 hours | |

| 10 hours | |

| 10 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite