|

|

|

|

|||||

|

|

|

Note: The following is an excerpt from this week’s Earnings Trends report. You can access the full report that contains detailed historical actual and estimates for the current and following periods, please click here>>>

Here are the key points:

The Magnificent 7 stocks have lost ground lately, with the DeepSeek breakthrough putting a spotlight on the group’s ever-rising capital outlays that many in the market were already uncomfortable with.

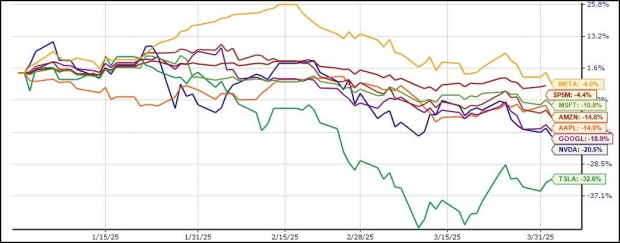

The chart below shows the year-to-date performance of these 7 stocks relative to the S&P 500 index.

As you can see here, Meta Platforms META is the only member of the group close to positive territory in 2025, outperforming the S&P 500 index (down -4.4%), while Tesla TSLA is at the bottom, having lost roughly a third of its value.

The rest of the group falls somewhere in the middle of the Meta and Tesla extremes, with Nvidia NVDA and Alphabet GOOGL positioned toward the bottom of the list, while Microsoft MSFT, Amazon AMZN, and Apple AAPL are located in the top half.

With respect to Tesla’s underperformance, it is tempting to blame Elon Musk’s political activities for becoming a headwind for the stock. But there is no shortage of fundamental issues related to the company’s China exposure, trade/tariff vulnerabilities, and the evolving EV competitive landscape that has to also be at play here. Apple is another member of the group that has significant exposure to both China and the trade and tariff issues.

Beyond Tesla and Apple, the outlook for the remaining five members of the group is closely tied to the overall sentiment on the artificial intelligence theme. All stocks related to this broad AI theme have been under a cloud lately, but these AI leaders are particularly vulnerable to this development given their heavy spending on the effort.

One key aspect of the Mag 7 group’s earlier market leadership was its enormous earnings power and strong growth profile. The earnings outlook for the group was consistently positive last year, with analysts steadily raising their estimates.

Our analysis of evolving earnings estimates for the group indicates that the outlook is significantly less positive than it had been in the recent past.

For 2025 Q1, the expectation is that Mag 7 earnings will increase +13.1% on +11.7% higher revenues. This would follow the group’s +31.0% earnings growth on +12.8% revenue growth in the preceding period.

For calendar year 2025, the expectation is that Mag 7 earnings will increase +12.6% on +9.3% higher revenues. This would follow the group’s +40.4% earnings growth on +16.8% revenue growth in 2024.

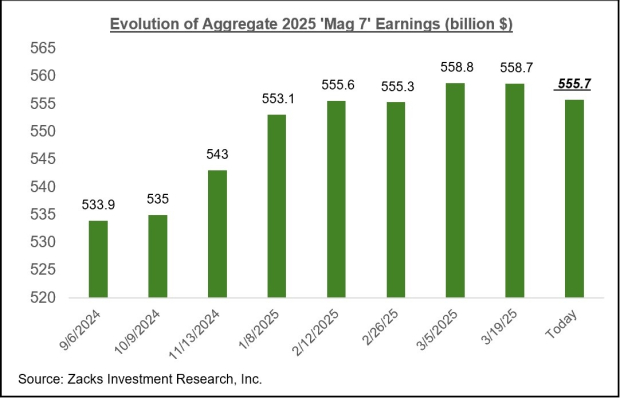

In the aggregate, the Mag 7 group is expected to bring in $555.7 billion in earnings, up from the 2024 aggregate total of $493.7 billion. The chart below shows how the aggregate 2025 earnings total has evolved in recent months.

The levelling out of the revisions trend in the above chart reflects how estimates for Tesla, Apple, and Meta have been unfolding in recent days, with the outlook for the rest of the group still very much positive.

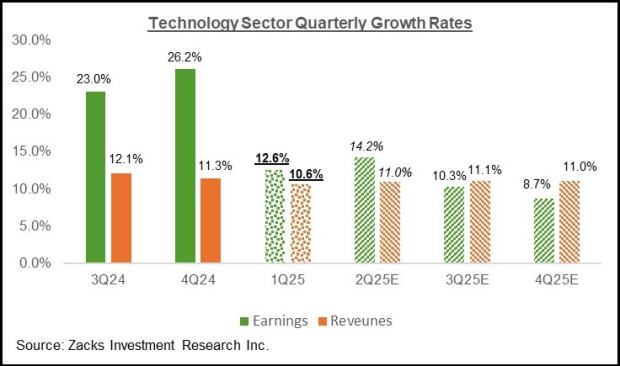

The Tech sector has been a significant growth driver in recent quarters, and we saw the same trend at play in 2024 Q4. For Q1, Tech sector earnings are expected to be up +12.6% from the same period last year on +10.6% higher revenues, the 7th quarter in a row of double-digit earnings growth.

This would follow the sector’s +26.2% earnings growth on +11.3% higher revenues in 2024 Q4. As the chart below shows, the sector’s growth trajectory is expected to continue in the coming quarters.

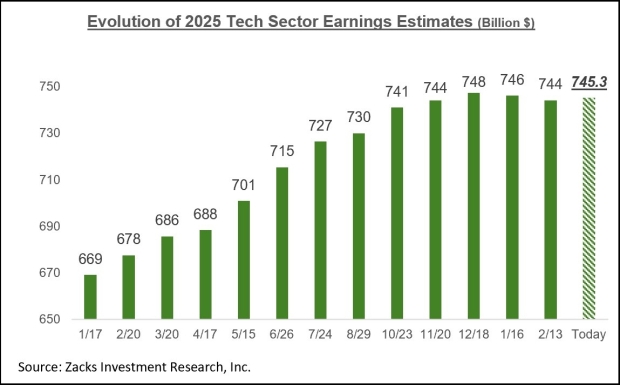

The Tech sector has also been among the few sectors that have steadily enjoyed an improving earnings outlook, with estimates increasing steadily over the past year. However, the more recent data on this count shows a shift in the revisions trend, with estimates for Q1 modestly under pressure since January, though they remain positive for the full year of 2025. This is evident in the chart below, which shows the aggregate 2025 earnings estimates for the sector.

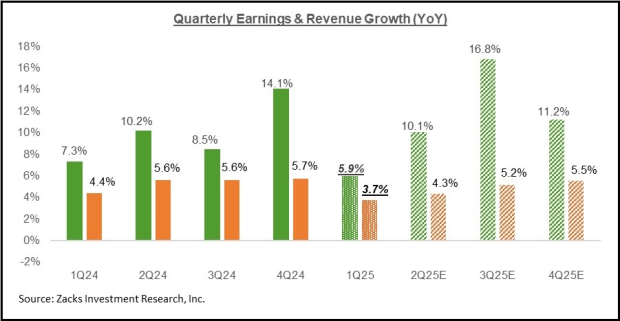

The chart below shows expectations for 2025 Q1 in terms of what was achieved in the preceding four periods and what is currently expected for the next three quarters.

As you can see in the above chart, total S&P 500 earnings for the current period (2025 Q1) are currently expected to be up +5.9% from the same period last year on +3.7% higher revenues.

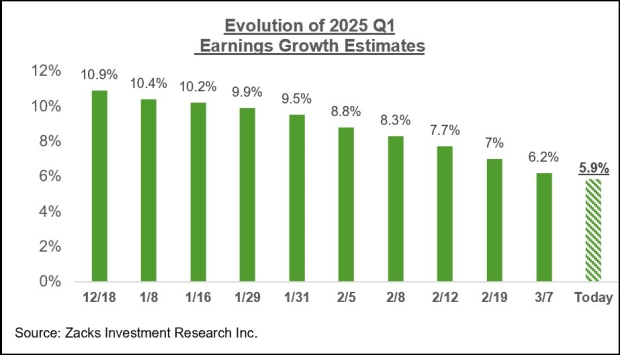

Estimates for the period have been coming down since the quarter got underway, as the chart below shows.

The revisions trend is broad-based, with estimates for 14 of the 16 sectors down since the start of January (Medical and Construction are the only sectors whose estimates have increased). Sectors suffering the most significant cuts to estimates include Conglomerates, Aerospace, Construction, Basic Materials, Autos, and others. Unlike other recent periods, estimates for the Tech sector have also been under pressure.

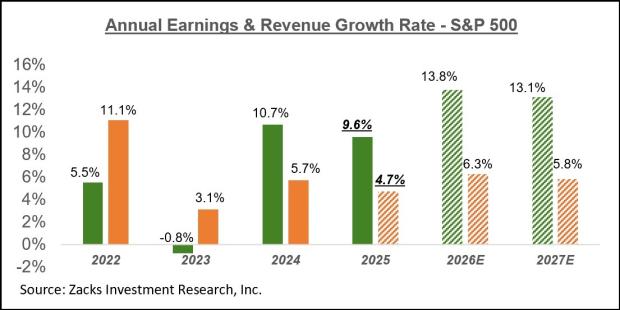

The chart below shows the overall earnings picture on an annual basis.

As you can see, the expectation is for double-digit earnings growth in each of the next two years, with the number of sectors enjoying strong growth notably expanding from the narrow base we have been seeing lately.

We should keep in mind, however, that these expectations will most likely be adjusted downward as the effects of slowing U.S. economic growth and tariffs begin to be reflected in diminished corporate profitability.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 24 min | |

| 38 min | |

| 48 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite