|

|

|

|

|||||

|

|

|

West Pharmaceutical Services, Inc. WST is well-positioned for growth, backed by the robust GLP-1-related demand and expansion plans. However, pricing headwinds and tariff risks are concerning.

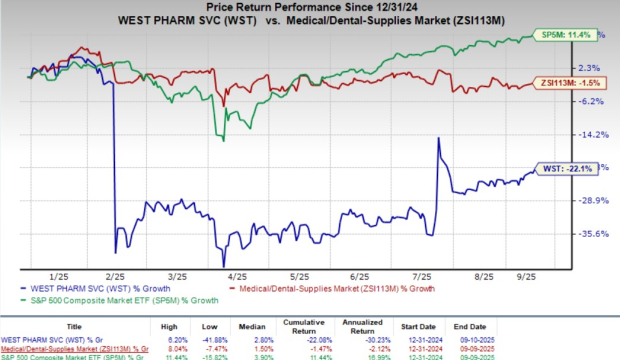

Shares of this Zacks Rank #1 (Strong Buy) company have lost 22.1% so far this year compared with the industry's 1.5% decline. The S&P 500 Index has increased 11.4% in the same time frame.

West Pharmaceutical, with a market capitalization of $18.1 billion, is a leading global manufacturer, engaged in the design and production of technologically advanced, high-quality, integrated containment and delivery systems for injectable drugs and healthcare products. Its earnings are anticipated to improve 8.4% over the next five years. The company delivered a trailing four-quarter average earnings surprise of 16.81%.

Let’s delve deeper.

Strength in GLP-1 Related Demand: WST’s high-value product (HVP) components tied to GLP-1 therapies (notably used in obesity and diabetes treatments) are performing well. These accounted for about 8% of second-quarter revenues and continue to grow. Additionally, the GLP-1 auto-injector business within the Contract Manufacturing segment is ramping up, helping offset revenue loss from CGM contract exits. The company has also repurposed COVID-era infrastructure to support this GLP-1 growth, enhancing capital efficiency.

Expansion Opportunities: Annex 1-related projects (focused on sterile manufacturing compliance in Europe) are contributing meaningfully, with 370 active customer projects versus 340 last quarter. This initiative is driving a favorable mix shift toward premium-margin HVP offerings, particularly within the standard and generic pharma categories, which could materially boost growth and margins in the coming quarters, even if its current revenue contribution remains modest.

Operational Efficiency and Margin Management:Despite pricing pressure and a temporary supply constraint at one facility, WST is maintaining margins through improved operational efficiency, restructuring actions and SG&A control. Automation of SmartDose production (expected late 2025/early 2026) is a long-term lever to improve margins in delivery devices. WST has also reaffirmed its capital allocation strategy toward margin-accretive investments and shareholder returns, further supporting EPS upside.

West Pharmaceutical Services is facing a combination of margin pressure, pricing headwinds, and tariff-related risks that could weigh on its performance through the remainder of 2025.

A significant source of margin pressure is the shift in product mix — specifically, growth in lower-margin delivery devices like SmartDose and contract manufacturing projects, which are diluting the profitability of high-value components such as FluroTec. While initiatives like automation are underway to improve cost efficiency, their benefits may not materialize until late 2025 or early 2026.

Adding to this, WST has flagged softer-than-expected pricing realization for the full year. Although price increases contributed meaningfully to first-quarter revenue growth, management now anticipates lighter pricing contributions going forward, reflecting both customer dynamics and competitive pressures.

In addition to these internal challenges, the company faces external headwinds from evolving geopolitical risks. Newly imposed tariffs are projected to create a $15-$20 million cost burden for full-year 2025, with uncertainty around potential retaliatory actions.

While WST is actively pursuing mitigation strategies, including possible cost pass-throughs, these are not yet reflected in its updated guidance. These factors, in unison, cause earnings volatility and constrain the company’s ability to fully leverage demand momentum.

WST has been witnessing a positive estimate revision for 2025. In the past 60 days, the Zacks Consensus Estimate for earnings has moved north from $6.28 at $6.74 per share, implying a decline of 0.2% from the prior-year level. The consensus mark for revenues is pegged at $3.03 billion, indicating a 4.7% increase from the 2024 level.

West Pharmaceutical Services, Inc. price | West Pharmaceutical Services, Inc. Quote

Some other top-ranked stocks from the same medical industry are Medspace MEDP, GE HealthCare Technologies GEHC and Inogen INGN.

Medspace, sporting a Zacks Rank of 1 at present, has an estimated growth rate of 11.4% for the next five years. You can see the complete list of today’s Zacks #1 Rank stocks here.

MEDP’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 13.87%. MEDP’s shares have gained 43.5% so far this year.

GE HealthCare, carrying a Zacks Rank #2 (Buy) at present, has an estimated growth rate of 5.8% for the next five years.

GEHC’s earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 12.53%. GE HealthCare’s shares have fallen 2.8% year to date.

Inogen, carrying a Zacks Rank of 2 at present, has an estimated earnings growth rate of 37.5% for 2025.

INGN’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 40.70%. Inogen’s shares have declined 9.3% so far this year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite