|

|

|

|

|||||

|

|

|

As Costco Wholesale Corporation COST prepares to unveil its first-quarter fiscal 2026 earnings results on Dec. 11, after the market closes, investors face an important decision: Should they buy the stock now or hold their current positions? With earnings expectations and market conditions in mind, it is crucial to evaluate key factors influencing Costco’s performance and whether the stock offers an attractive entry point ahead of its earnings report.

Costco's strategic investments, customer-centric approach, merchandise initiatives and focus on membership growth have enabled it to navigate the market. These strengths have resulted in decent sales and earnings growth, positioning COST as a consumer defensive stock.

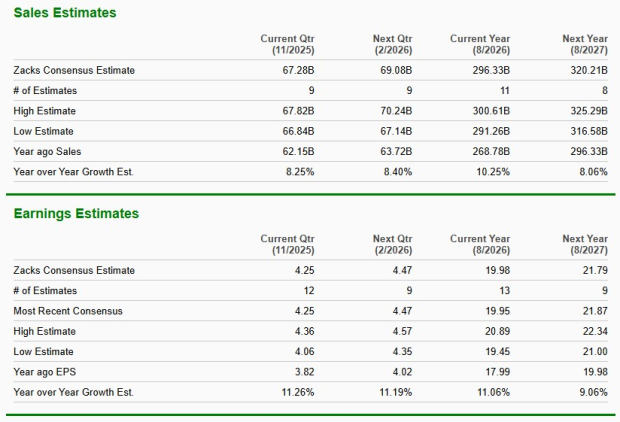

Analysts are optimistic about Costco's upcoming earnings. The Zacks Consensus Estimate for first-quarter revenues stands at $67.28 billion, calling for an 8.3% increase from the prior-year reported figure. On the earnings front, the consensus estimate has improved by a penny to $4.25 per share over the past seven days, implying an 11.3% year-over-year jump.

Costco has a trailing four-quarter earnings surprise of 0.2%, on average. In the last reported quarter, this Issaquah, WA-based company beat the Zacks Consensus Estimate by a margin of 1%.

As investors prepare for Costco's first-quarter announcement, the question looms regarding earnings beat or miss. Our proven model predicts that an earnings beat is likely for Costco this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

Costco has an Earnings ESP of +0.47% and carries a Zacks Rank #3. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Costco Wholesale Corporation price-consensus-eps-surprise-chart | Costco Wholesale Corporation Quote

Costco’s growth strategies, competitive pricing and membership-driven business model have been instrumental in its sustained success. By offering products at discounted rates, the company appeals to shoppers seeking value and convenience. The company's bulk purchasing power and efficient inventory management allow it to keep prices low. This disciplined pricing mechanism helps Costco maintain steady store traffic and robust sales volumes. These factors are expected to have a favorable impact on the overall results.

Costco, in its latest November sales report, highlighted that net sales for the 12-week first quarter ended Nov. 23, 2025 reached $65.98 billion, reflecting an 8.2% increase from $60.99 billion last year. This growth was supported by strong comparable sales gains across regions and a notable contribution from e-commerce channels. Total comparable sales for the quarter rose 6.4%, supported by gains of 5.9% in the United States, 6.5% in Canada and 8.8% in Other International markets.

Furthermore, an expanding membership base, rising penetration of higher-value Executive memberships and a younger cohort entering the system all point to a robust membership fee income. Costco is promoting auto-renewal, enhancing targeted digital communication, and adding new member benefits such as extended warehouse hours and a $10 monthly Instacart credit for Executive members to strengthen engagement and reinforce loyalty. We expect membership fees to increase 11.3% during the quarter under review.

Costco continuously evolves to meet shifting market demands, regularly updating its product portfolio to include everyday necessities and unique, high-demand items to appeal to diverse customer groups. At the same time, ongoing investments in technology and logistics are reinforcing a seamless multi-channel ecosystem. Digitally enabled comparable sales rose 20.5% in the first quarter.

With a clear emphasis on delivering value-oriented offerings, Costco remains well-positioned for continued success in the dynamic retail landscape. However, it is essential to acknowledge the presence of certain headwinds, including underlying inflationary pressures, which may pose challenges. Moreover, margins remain a critical area to monitor, with potential concerns stemming from any deleverage in the SG&A rate. We expect SG&A expenses to increase 8.5% year over year.

Costco, which competes with Dollar General Corporation DG, Ross Stores, Inc. ROST and Target Corporation TGT, has seen its shares decline 10.6% in the past year compared with the industry’s fall of 0.1%. While shares of Dollar General and Ross Stores have rallied 51.3% and 14.3%, respectively, those of Target have dropped 30.9% in the aforementioned period.

From a valuation standpoint, Costco currently trades at a premium relative to its industry peers. The company’s forward 12-month price-to-earnings (P/E) ratio is 43.71, higher than the industry average of 30.16 and the S&P 500’s 23.59. However, the stock is also trading below its median P/E level of 49.87, observed over the past year. This valuation suggests that while Costco trades below its historical peak, investors are paying a premium relative to the company’s anticipated earnings growth.

Costco is trading at a premium to Target (with a forward 12-month P/E ratio of 12.03), Ross Stores (25.57) and Dollar General (19.73).

Costco has strengthened its position as a retail powerhouse, thanks to its strong membership model, competitive pricing and ability to adapt to evolving market trends. While the stock’s premium valuation might deter some investors, its steady growth, robust financial health and strategic initiatives indicate the potential for further upside. Current investors may consider holding or adding to their positions, while prospective investors could see any dips as a buying opportunity.

Costco is heading into its first-quarter report with positive momentum, setting the stage for a potential earnings beat. Despite the stock’s high valuation and recent underperformance, factors such as consistent traffic, strong membership growth and effective operations indicate that Costco remains a reliable investment option ahead of the earnings release. For those considering investing in Costco, the current backdrop suggests that initiating positions ahead of the earnings release may be reasonable if one is seeking stability, even though short-term volatility may be expected. Meanwhile, existing shareholders may find it prudent to maintain their positions, as the underlying business fundamentals and favorable earnings setup provide enough support to weather any market fluctuations following the announcement.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 9 hours | |

| 11 hours | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite