|

|

|

|

|||||

|

|

|

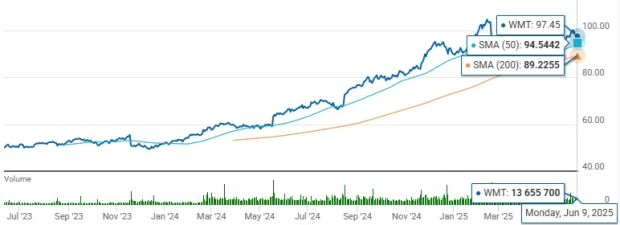

Walmart Inc. WMT continues to lead the retail space with its diversified business model, robust omnichannel presence and advanced retail capabilities. These strengths have positioned the company well in an evolving retail landscape. However, Walmart’s current forward 12-month price-to-earnings (P/E) ratio of 36.07X raises valuation concerns. This figure is significantly higher than the Zacks Retail - Supermarkets industry’s average of 33.07X and the S&P 500’s average of 21.96X, making WMT stock appear relatively expensive.

When compared to key retail peers, Walmart’s valuation looks even steeper. For instance, The Kroger Co. KR trades at 13.54X, Target Corporation TGT at 12.63X, and Ross Stores, Inc. ROST at 22.14X — all notably lower than Walmart’s multiple. Moreover, WMT holds a Zacks Value Score of C, signaling a limited value appeal at current price levels.

Despite this, investor optimism around Walmart remains robust, thanks to its consistent growth and strong fundamentals. Over the past three months, WMT shares have surged 11.4%, outpacing the industry (+10.7%), the broader Zacks Retail – Wholesale sector (+6.3%), and the S&P 500 (+7.5%). In contrast, Kroger and Target stocks have declined 1.6% and 13.7%, respectively, while Ross Stores gained 10.5% during this time.

Adding to the bullish sentiment, Walmart trades above both its 50-day and 200-day moving averages, indicating sustained momentum and investor confidence. These technical indicators reinforce the stock's upward trend and price stability.

Given these dynamics, investors should weigh Walmart’s strong growth potential against its elevated valuation before making a decision.

Walmart continues to thrive on the back of its robust, diversified business model and consistent performance across segments, geographies, and sales channels. The retail giant is successfully capturing increased customer traffic both in-store and online, highlighting its ability to evolve with the changing dynamics of the global retail industry. With a multi-channel revenue strategy — spanning physical retail, e-commerce, advertising, and memberships — Walmart is building a solid foundation for sustained long-term growth.

A core driver of Walmart’s momentum is its powerful omnichannel ecosystem, which seamlessly integrates brick-and-mortar locations with digital capabilities. The company is leveraging data analytics, technology investments, and in-store operational enhancements to deliver a superior customer experience. With the majority of Americans living close to a Walmart store, the retailer can efficiently fulfill online orders through store-based logistics, offering speed and convenience. Retail giants such as Kroger, Target and Ross Stores are also advancing in omnichannel strategies, underscoring the industry’s pivot toward this model.

Meanwhile, Walmart has made significant strides in strengthening its e-commerce operations. Strategic acquisitions, tech upgrades, and delivery partnerships have fueled growth. In the first quarter of fiscal 2026, global e-commerce sales surged 22%, led by strong adoption across all business segments. In the United States, e-commerce sales jumped 21%, driven by fast fulfillment, robust marketplace activity, and growing advertising revenues. International e-commerce rose 20%, while Sam’s Club U.S. saw a 27% spike, fueled by growth in club-fulfilled delivery and pickup services.

The company also reported impressive comparable sales growth, underpinned by ongoing store upgrades and digital innovations. U.S. comparable sales (excluding fuel) rose 4.5%, with a 1.6% increase in transactions and a 2.8% rise in average ticket size, reflecting strong consumer engagement and value-driven shopping behavior. The grocery segment remained a standout, achieving mid-single-digit comp sales growth and expanding market share.

Walmart is now intensifying its focus on high-margin revenue streams, including advertising, membership programs, and marketplace expansion. Key growth engines like Walmart Connect (its advertising platform) and Walmart+ (its subscription-based membership offering) are delivering robust results. In the fiscal first quarter, advertising revenues soared 50%, while membership income climbed 14.8%, showcasing the success of Walmart’s shift toward tech-enabled, margin-accretive services that boost customer loyalty and earnings quality.

While Walmart continues to demonstrate strong operational momentum, the company is facing increasing challenges from tariff pressures that could weigh on near-term financial results. On its last earnings call, the company acknowledged it is not fully immune to the short-term effects of ongoing tariffs, warning that a return to sharply higher tariff levels could jeopardize its ability to grow earnings year over year. Management also withheld second-quarter fiscal 2026 earnings per share (EPS) guidance, citing a highly fluid environment and the difficulty of forecasting amid ongoing volatility.

In addition to tariff concerns, Walmart has substantial exposure to global markets, making it vulnerable to foreign exchange fluctuations. In first-quarter fiscal 2026 alone, unfavorable foreign exchange rates reduced reported sales by $2.4 billion. Together, these external pressures introduce a layer of uncertainty into Walmart’s near-term outlook, even as its core business remains fundamentally strong.

The Zacks Consensus Estimate for Walmart’s EPS for the current fiscal year has dipped by one cent over the past 30 days, now standing at $2.59. Despite the minor downward revision, the estimate still suggests a 3.2% year-over-year increase, signaling modest earnings growth for Walmart in fiscal 2026.

For investors, Walmart presents a compelling mix of long-term growth potential and near-term valuation caution. While the stock trades at a premium compared to industry peers, its strong omnichannel strategy, expanding high-margin revenue streams, and consistent comparable sales growth offer solid upside. However, macroeconomic risks like tariffs and currency fluctuations could put pressure on short-term performance. For long-term holders, the fundamentals remain compelling — yet those seeking value may prefer to wait for a better entry point.

At present, WMT carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Indian payments firms flag competition risks in one-click UPI checkout- report

WMT

Electronic Payments

|

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite