|

|

|

|

|||||

|

|

|

SoundHound AI SOUN continues to command a rich valuation. The company’s forward 12-month price-to-sales (P/S) ratio stands at 20.45, above the Zacks Computers - IT Services industry average of 19.17. Over the past three years, SOUN’s P/S ratio has fluctuated widely between 2.92 and 94.4, showing how investor appetite for voice AI has shifted depending on macro conditions and competitive progress.

SoundHound has quickly emerged as a key player in conversational AI, gaining traction in the automotive and restaurant sectors with its proprietary voice platform. Yet, the stock’s lofty valuation metrics and stiff competition from Big Tech are keeping many investors cautious.

SOUN’s Valuation

In the past three months, shares of SoundHound have slipped 1.7%, underperforming the industry’s 6.3% gain. It also trailed the broader Zacks Computer and Technology sector’s 11.2% increase and the S&P 500’s 5.7% climb over the same period.

While the stock currently trades at a 62.3% discount to its 52-week high of $24.98, it remains well above its low of $3.82, suggesting that investor sentiment is still tied to long-term growth expectations rather than near-term earnings delivery.

As shares trade significantly off their 52-week highs but remain priced at a premium, the big question is whether SoundHound’s growth story still justifies the tag. Let's analyze.

SOUN Stock Performance

The core of SoundHound’s investment case lies in its expanding Polaris platform and the recently launched agentic AI offering, Amelia 7.0. Polaris enables real-time voice recognition in noisy environments like vehicles and restaurants, while Amelia takes the platform a step further by adding autonomous task execution, allowing users to complete transactions via voice, such as ordering food or booking services.

The company’s voice AI solutions have already been adopted at over 13,000 restaurant locations. A recent partnership with Mastercard marks its entry into AI-enabled payment flows, positioning SoundHound to tap into broader commerce trends. On the automotive front, its solutions are now being piloted or deployed by several OEMs across the United States, Europe, and Asia.

A major tailwind is the rapid rise of the agentic AI market, autonomous AI agents capable of completing customer tasks without human intervention. SoundHound is leveraging this to enter verticals like healthcare, which is evident in its partnership with Allina Health, where its AI helps patients manage appointments and prescriptions. In 2023, the US healthcare market reached $4.9 trillion in spending, according to the American Medical Association. In 2025, the U.S. healthcare sector is set to represent a meaningful expansion opportunity, and SOUN is also expected to gain from the expansion.

SoundHound reported revenue of $29.1 million in the first quarter of 2025, marking a 151% year-over-year surge. This growth was led by increased adoption of its voice AI solutions across restaurants, automotive, enterprise, and other industries. Notably, the company activated over 1,000 new restaurant locations in the quarter, which is nearly 10 times the rate from a year ago, and now serves close to 13,000 locations. Enterprise clients also drove significant growth, with SoundHound handling five times more support tickets quarter over quarter and reducing resolution time by 50-fold through automation.

SoundHound reaffirmed its 2025 revenue guidance of $157–$177 million, expecting stronger revenue weighting in the first half—about 40%—versus the historical 30%. Adjusted EBITDA is expected to improve sequentially through 2025, with management reiterating its commitment to reaching profitability by year-end. The company ended the quarter with $246 million in cash and no debt, offering operational flexibility.

Despite operational momentum, SoundHound faces formidable competition from deep-pocketed tech giants. Alphabet GOOGL, Amazon AMZN, and Apple AAPL dominate the AI-powered voice assistant market. Google Assistant powers Android Automotive and is well integrated into in-car experiences globally. Amazon’s Alexa, backed by AWS and a large developer community, is expanding into vehicles and has an entrenched smart home base. Apple’s Siri benefits from tight integration across its ecosystem, especially via iPhones and CarPlay.

These companies not only have brand recognition and massive user networks, but they also enjoy platform lock-in that discourages customers from switching. For SoundHound to win, it must continue carving out niche capabilities and deliver more customizable, lightweight, and embeddable solutions than what Big Tech offers.

Adding to the pressure, the company faced softness in its automotive business due to geopolitical and macro uncertainties affecting global supply chains. Automotive ASPs rose, but unit volumes were under pressure. SoundHound still expects the sector to rebound as OEMs embrace voice commerce, but this remains a near-term headwind.

Margin pressures also persisted due to integration costs from acquisitions and legacy contracts with suboptimal profitability. While management is working to phase these out over 18–24 months, gross margin variability will likely be in the near term.

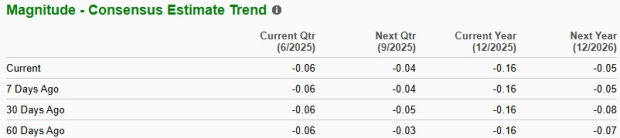

The unchanged Zacks Consensus Estimate for a full-year loss in 2025 further limits near-term upside, even though the expected loss reflects improvement from the previous year’s $1.04 per share. The muted estimate revisions also indicate a lack of new catalysts or surprises that could prompt analysts to upgrade the stock soon.

SoundHound’s stock continues to trade at a premium despite recent underperformance. The company’s expanding Polaris platform and new agentic AI offering, Amelia 7.0, are gaining meaningful traction across high-value sectors like restaurants, automotive, and healthcare. While competitive pressure from Big Tech remains intense and gross margins face temporary pressure, SoundHound’s consistent revenue momentum, debt-free balance sheet, and reaffirmed profitability guidance by year-end 2025 offer important stability.

The muted stock price action and stagnant estimate revisions suggest that near-term gains may be capped. However, with a robust pipeline, rising voice AI adoption, and a discounted price from 52-week highs, the stock appears fairly valued for those with a longer-term outlook. SoundHound currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 30 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite